NCLT Chandigarh (2025.07.02) in Tajinder Pal Setia Vs. Sh. Arvind Kumar (RP) and Ors. [(2025) ibclaw.in 873 NCLT, IA (I.B.C)/2105(CH)2023 in CP(IB) No. 248/Chd/Chd/2019] held that;

We do not find any merit in the submission of the Applicant that the claim of the Respondent Nos. 2 and 3 are liable to be rejected as the same do not appear in the audited balance sheets. Balance sheet is not the sole basis for proving or admission of claim. Hence, mere non reflection of the claim amount in the Balance Sheet cannot be the sole ground of rejection.

Thus, it becomes clear that whether the homebuyer/ allottee is genuine homebuyer or genuine allottee or speculative homebuyers/ allottee but if he has paid the money for acquisition of such properties or given the advance, such allottee/ homebuyer shall be treated as Financial Creditor in terms of Section 5(8)(f) of the Code

In our view the Speculative Investor is barred from initating the CIR Process. However, we don’t find any impediment to treat the Allottees, even if they are speculative investors, from filing their claim and admission of their claim as Financial Creditor in a class. The claim of an allottee cannot be extinguished merely because of being a Speculative Investor.

As such, the financial creditor who in praesenti is not a related party, would not be debarred from being a member of the CoC. However, in case where the related party financial creditor divests itself of its shareholding or ceases to become a related party in a business capacity with the sole intention of participating the CoC and sabotage the CIRP, by diluting the vote share of other creditors or otherwise, it would be in keeping with the object and purpose of the first proviso to Section 21(2), to consider the former related party creditor, as one debarred under the first proviso.

Excerpts of the Order;

The present Application has been filed by Mr. Tejinder Pal Setia, Suspended Director of Chandigarh Overseas Private Limited (“Corporate Debtor” or “CD”) under ection 60(5) read with Section 21 of Insolvency and Bankruptcy Code (“IBC”) seeking to exclude Respondent No. 2 and 3 from the Committee of Creditors (“CoC”) on the ground that they are neither Financial Creditors nor Class of Creditors- Homebuyers/Allottees, as they are business partners/service providers and cannot be treated as homebuyers and are speculative investors and with a prayer to reconstitute the CoC and declare all the actions and decisions including the resolutions passed in1st CoC meeting dated 03.08.2023 as illegal. A further prayer has been made that affairs of the Respondent Nos. 2 and 3 be inquired/investigated by Proforma Respondents 4-7, i.e. jurisdictional Department of Income Tax and Registrar of Companies.

2) The Respondent No. 1 had earlier filed Reply vide Diary No. 2967/1 dated 26.9.2023 and was later permitted to file an Updated Reply vide order dated 4.1.2024, in compliance with which, Updated Reply was filed vide Diary No. 2967/11 dated 15.1.2024. Replies have also been filed by Respondent Nos. 2 & 3 vide Diary No. 2967/2 dated 3.10.23 and Diary No.2967/3 dated 4.10.23 respectively. The Applicant has filed Rejoinder to Replies vide Diary No. 2967/4 dated 04.10.2023, Diary Nos. 2967/5 and Diary No. 2967/6 dated 10.10.2023. Respondent Nos. 2 and 3 have filed further Replies vide Diary Nos. 2967/7 and 2967/8 dated 16.10.2023. The Respondent Nos. 4-7 have not entered appearance. The parties have also filed their respective Short Notes.

3) The Applicant had also filed IA No. 2209/2023 to place on record additional documents in the present IA, which was allowed subject to just exceptions vide order dated 09.05.2024.

4) BRIEF FACTS: The uncontroverted chronological facts in brief are as under:

SUBMISSIONS OF THE APPLICANT

5) The Respondent No. 2 and 3 are not homebuyers/allottees/Financial Creditors nor are they entitled to be part of COC. They are business partners, developers, speculative investors and interested only in the profit the project and are not homebuyers. Their business terms are completely different as compared to other allottees. Further, Inflated and exaggerated claims have been admitted by the RP for oblique motive contrary to records of the CD and on the basis of unsubstantiated, inadmissible and illegal documents.

6) The affairs of Respondent No. 2 and 3 including their directors and shareholders, be inquired and investigated by Respondent Nos. 4 to 7.

7) It has been further averred as under:

i. The RP has admitted the claim on the basis of a receipt dated 31.12.2023 for Rs. 20,52,32,957/- wherein the said amount has been shown as paid through cheque and cash collectively with no bifurcation with respect to the cash and cheque. Moreover, an amount of Rs. 9,96,50,000/- paid by the respondent no. 2 has already been exhausted against the sale deeds executed and therefore, the said amount should not have been part of the claim. The said receipt is executed by ex- director of CD (who also happens to be common director in another company with director of R-2). The description of property is also termed as “ACCORD HIGH STREET” in the said sale deeds.

ii. The audited Balance Sheet of Respondent no. 2 as on 31.03.2014, which happens to be for the period after the said alleged receipt was made, neither support the said claim nor the investments made by the respondent no. 2 with the applicant as the total of the Balance Sheet i.e., 7.10 Crores of Rupees, itself does not cover the amount as mentioned in the said receipt of Rs. 20.52 Crores of Rupees. Therefore, the said receipt is false, fabricated and back-dated. iii. The claim of Respondent No. 2 has been admitted at Rs. 31,30,40,054/- whereas Rs. 5,39,21,712/- is recoverable from it.

iv. The Applicant has also submitted that the books of accounts were provided to the RP on 31.07.2023.

v. The Respondent no(s) 2 and 3 were speculative investors and are not genuine home buyers and hence, their claims cannot be admitted.

vi. The RP has wrongly admitted the Claim of Respondent No. 2 based on Agreement dated 24.06.2011 with the CD as under the said Agreement the said Respondent was to market and sell the properties constructed by the CD, issue allotment letters, receive payments and to execute buyer-seller agreements and other documents and hence, is a speculative investor and is not covered within the definition of a financial creditor as a home buyer.

vii. The another Agreement to Sell dated 26.02.2012 was executed between Respondent No. 2 and the CD which stated that the properties will be built by the CD and handed over to the respondent who will have right to further sell the property, hence the said Respondent is a speculative investor and is not covered within the definition of a financial creditor as a home buyer.

viii. The Respondent No. 2 had been marketing the properties allotted to it by the CD and on a complaint by a buyer from the said respondent, District Consumer Disputes Redressal Forum, Chandigarh had directed refund against the said respondent, which shows that the said Respondent is a speculative investor and is not covered within the definition of a financial creditor as a home buyer.

ix. There was collusion between the ex-directors of CD and director of Respondent No. 2 as both were common directors in Sarv Awas Housing Bhiwadi Private Limited which is currently in CIRP and hence, Respondent No. 2 is a related party.

x. The applicant further submitted that the name of the respondents 2 & 3 company was struck off under Section 248 of the Companies Act, 2013 for non-filing of financial statements and hence cannot file claim.

xi. The Respondent No. 2 has made cash payments to the CD and as per Section 269SS of the Income Tax Act, such transactions are barred.

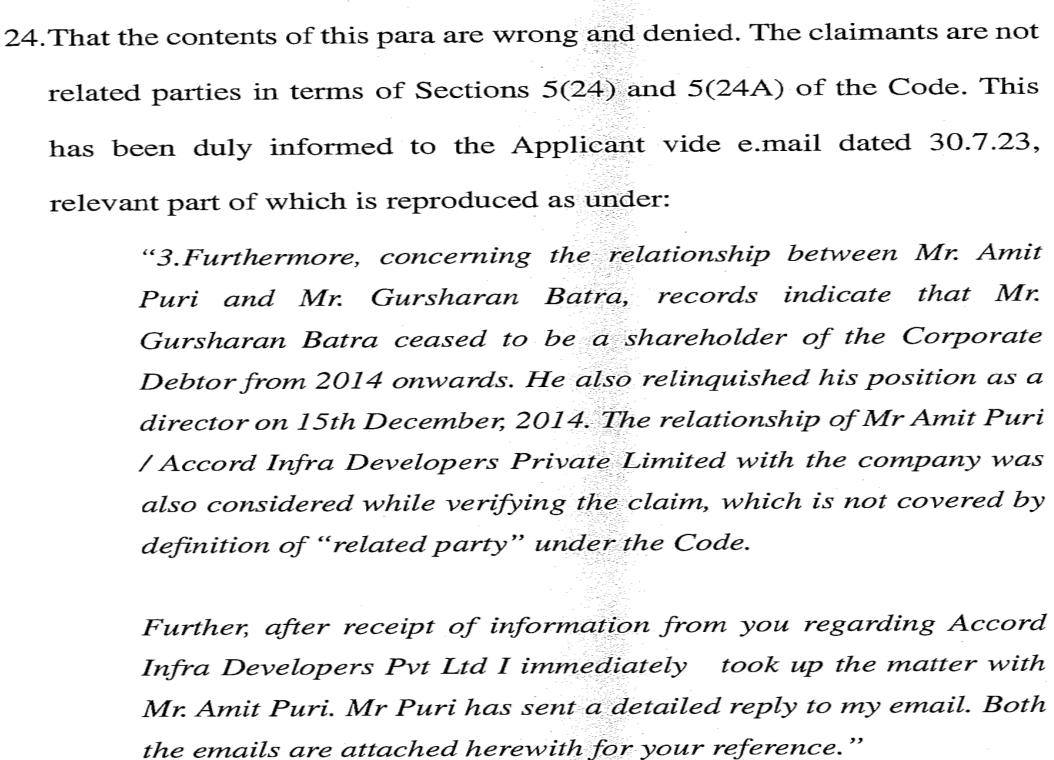

xii. The claim of the Respondents is time barred.

8) With regard to Respondent No. 3, it has been averred that an Agreement dated 29.06.2009 was entered into between the said respondent and the CD wherein the Respondent No. 2 has been referred to as promoter and the CD has been referred to as developer and the said Respondent had agreed to buy 40 residential units and 40 industrial units and the respondent could sell the properties and sign builder buyer agreement. It has further been averred that as per Ledger of CD Rs. 3.41 crore is payable to Respondent No. 3 whereas a claim of Rs. 28.21 Crores has been admitted by the RP without any basis.

9) The balance sheet of the CD doesn’t reflect the names or amounts of claims which have been admitted by the RP.

10) It has further been averred that the Applicant has the locus to maintain the present application and this Adjudicating Authority has power to order for inquiry into the affairs of the Respondents.

11) In support of his averments, the Applicant has placed reliance on the following judgments:

i. Pioneer Urban Land & Infrastructure v. Union of India: 2019 [8) SCC 416.

ii. M/s Jagbasera infrastructure Pvt. Ltd. v. Rawal Variety Construction Ltd. : NCLAT: CA(AT)(Ins.) 150 of 2019: D/d- 04.04.2022.

iii. Vipul Ltd. v. M/s Solitaire Buildmart Ltd.: NCLAT: CA (AT) (Ins.) 550 of 2020 : D/d- 18.08.2020.

iv. Mohit Prasad v. M/s S & N Lifestyle Infrastructure Pvt. Ltd.: NCLT (New Delhi): CP(IB) 1026 of 2020: D/d- 28.03.2023.

v. Mukesh N. Desai v. Piyush Patel & Ors.: NCLAT: CA(AT)(Ins.) 780 of 2020: D/d- 24.02.2022.

vi. Nidhi Rekhan v. M/s Samyak Projects Pvt. Ltd.: NCLAT: CA(AT) (Ins.) 1035 of 2020: D/d- 31.01.2022.

vii. Budhpur Buildcon Pvt. Ltd. v. Abhay Narayan Manudhare: NCLAT: CA (AT) (Ins.) 589 of 2021: D/d-09.09.2022.

SUBMISSIONS BY RESPONDENT NO. 1 RP

12) At the outset, the RP has averred that the Applicant is a chronic litigant and is trying to disrupt the CIRP and has raised preliminary objection on the maintainability of the Application on the ground of res judicata and unclean hands of the Applicant as under:

i. Another suspended director, Jagbir Singh had filed IA No. 1571/2023 inter alia seeking to place on record a Forensic Audit Report inter alia disputing the claims of Respondent Nos. 2 and 3 and the same was dismissed by this Adjudicating Authority vide orders dated 27.07.2023.

ii. The Applicant, Tejinder Pal Setia had filed Civil Appeal Nos. 5533-34 of 2023 before the Hon’ble Supreme Court (against judgment of Hon’ble NCLAT dated 23.8.2023) wherein the Grounds of appeal, similar grievances have been raised as in the present Application (Annexure R-1/2).

iii. The Respondent No. 2 and 3 herein, who’s claims are being challenged by the Applicant were also arrayed as Respondent Nos. 54 and 55 respectively in the said Civil Appeal and;

iv. These facts have not been disclosed in the present Application and accordingly, the Applicant is guilty of suppression of material facts and forum shopping.

13) It has further been averred as under:

i. After initiation of the CIRP, the claim of the R2 and R3 were accepted based on the claim documents in the absence of any other information/data as per regulation 14(1). The CoC was constituted on 27.07.2023 by which time the suspended directors had not provided any records/books of accounts relating to the CD. On receipt of further claims, the Coc was reconstituted on 04.09.2023. Thereafter, the suspended management provided the books of account, bank account statements and other records on 17.09.2023, based on this fresh information, the existing claims were revised under regulation 14 (2).

ii. As and when direct claims from buyers of units from R-2 and R-3 were filed, the same were collated and corresponding admitted claims of R-2 & R-3 were reduced. The claims were updated under regulation 14(2) and the CoC was constituted six times after its first constitution. The claims of R2 and R3 were as below on the dates of reconstitution of the CoC on various dates as per the following table (The authority intimate and available on website of IBBI):

*typographical error in updated reply at page 10 para 10 which totals Rs. 36,41,63,732 as the interest amount of 13,04,58,367 mentioned includes penalty and penalty of Rs. 5,11,23,678/- has been separately mentioned.

iii. Thus, the after 17.9.2023, ledger, bank account statements, books of accounts etc. of the CD has been duly considered for verification of the claims, including revision of existing claims.

iv. The allegations of the Applicant have been controverted and basis of admission of claims have been averred as under: . . . . . . . .

v. It has also been stated that the claims of the allottees have been collated as per the terms of the allotment letters/agreements and interest has been added to the claim as per Regulation 16A (7) (which is not reflected in the balance sheet) and penalty as per the Agreement.

vi. It has been averred that there is no anomaly in admission of the claims of the Respondent Nos. 2 and 3.

vii. As on date of approval of resolution plan on 19.03.2024, total number of claims of home-buyers is 365 valued at RS. 2,07,89,58, 476.31/- and value of claims of R-2 and R-3 is Rs. 8,82,33,357.77/- (voting share 4.21%) and 7,78,60,384/- (3.72%). The Plan was approved with 99.21% voting.

SUBMISSIONS BY RESPONDENT NOS. 2 AND 3

14) These Respondents have taken a similar stand that the Applicant has no locus standi and after the petition was admitted by this Adjudication Authority u/s 9 of the IBC on 27.2.2023, the Applicant has indulged into various litigations for closure of CIRP before Hon’ble NCLAT/Hon’ble Supreme Court having been unsuccessful, he is now trying the frustrate the CIRP proceedings.

15) They have further submitted that the Application is vexatious and is an attempt to threaten the respondents into withdrawing their claims as the Applicant have impleaded RoC/Income Tax Department as Proforma Respondents while seeking a prayer for inquiry/investigation by them into the affairs of these Respondents.

16) The Respondent No. 2 avers that it had initially entered into an Agreement dated 24.06.2011 with the CD, which was superseded by an Agreement to Sale dated 26.03.2012. As a consideration, a sum of Rs. 20,52,32,957/- has been paid by it to the CD towards which receipt dated 31.12.2023 was issued by the CD. The units sold to the respondent were not delivered by the CD and hence, claim was filed with the IRP.

17) The respondents have further stated that the audited balance sheet for the year 2020-21 (Annexure A-5), does not name any allottee as its creditors. However, the balance sheet shows a sum of Rs. 71,47,31,028/- under the head “Advance from customers. Similarly, the balance sheet for the year ended 31.03.2013 shows a sum of Rs. 70,84,90,632/- under the head “Advance from customer received against projects”. The Auditors Report for the year 2020-21 states as under:

18) It is stated that if the averment of the Applicant is to be accepted that only those allottees who’s name appear in the balance sheet, then all the other claims filed with the IRP/RP are null and void, which is not the case.

19) The Respondent No. 3 has further stated that it had issued a Legal Notice (Annexure R-3/0) dated 2.12.2015 to the CD by attaching Ledger Account of the CD showing payment of RS. 6.07 cr. and the CD did not respond to its legal notice and the Applicant has never challenged the Agreements entered into between the said respondent and the CD.

20) The allegation of the Applicant that the Agreements were entered into with the CD when the CD was under the old management is of no substance as it is the inner working of the CD. The Agreement is with the CD which is a separate entity than the management. As Respondent No. 2 had substantial interest in the project of the CD, its direct was a witness to the change of management Agreement dated 15.10.24 (Annexure R-2/9).

21) The Applicant had filed IA No. 1571 of 2023 under Section 12A of the IBC read with Regulation 30A of CIRP Regulations. The Respondents along with other had filed IA No. 1584/23 to be impleaded as Respondent Nos. 51 and 52. By way of order dated 25.7.2023, this Authority had allowed the intervention as necessary parties – Home buyers and eventually, IA 1571 was dismissed after hearing the respondents herein. This order was challenged by the Applicant before Hon’ble NCLAT and Hon’ble Supreme Court by way of Appeals, which were dismissed vide orders dated 23.8.23 and 6.9.2023 respectively. Hence, the Applicant cannot say that the respondents are not home buyers. W.r.t Respondent No. 3, when Applicant has admitted in paragraph

22 of the Application that a sum of Rs. 9,96,50,000/- has been received by the CD through banking channels.

22) The Respondents have a continuous cause of action as their Agreements have clause for damages for the delayed period of possession. As per RERA approval, the project was to be completed by 30.6.2022 (Annexure R- 2/11). Hence it is denied that the claim of respondents is time barred.

23) It is wrong to say that the respondents are shell companies merely on the ground that their name has been struck off by the RoC. Under Section 250 of the Companies Act, even if a company is dissolved under section 248, it can still realise the amount due to the company and for the payment or discharge of the liabilities or obligations of the company.

ANALYSIS AND FINDINGS

24) We have heard the parties and perused the record including the Written Submissions filed by both the parties. Through the present Application the Applicant who is member of Suspended Board of Directors has challenged the constitution of COC, i.e., inclusion of Respondent No.2 and 3 in the CoC

25) The Applicant has contended that the claim of the Respondents ought to be rejected as the same was not reflected in the Audited Balance Sheet of the Corporate Debtor. We would like to examine this contention of the Applicant. At this juncture we refer to Regulation 8A of CIRP Regulations which deals with manner of proving the claims by creditors in a class. It reads as under:

“(1) A person claiming to be a creditor in a class shall submit claim with proof to the interim resolution professional in electronic form in Form CA of the Schedule.

(2) The existence of debt due to a creditor in a class may be proved on the basis of-

(a) The records available with an information utility, if any; or

(b) Other relevant documents, including any-

(i) Agreement for sale;

(ii) Letter of allotment;

(iii) Receipt of payment made; or

(iv) Such other document, evidencing existence of debt.

(3) A creditor in a class may indicate its choice of an insolvency professional, from amongst the three choices provided by the interim resolution professional in the public announcement, to act as its authorised representative.”

26) We do not find any merit in the submission of the Applicant that the claim of the Respondent Nos. 2 and 3 are liable to be rejected as the same do not appear in the audited balance sheets. Balance sheet is not the sole basis for proving or admission of claim. Hence, mere non reflection of the claim amount in the Balance Sheet cannot be the sole ground of rejection.

27) The Applicant has contended that the respondent no. 2 & 3 are business partners, developers, speculative investors and interested only in the profit the project and are not homebuyers by referring to the Agreements dated 24.6.2011 and 26.3.2012 with Respondent No. 2 and Agreement dated 26.6.2029 & 29.8.2014 with Respondent No. 3. From these Agreements, it transpires that the units purchased by the Respondents will be constructed/developed by the CD and the said Respondents could sell/market the units and received consideration.

28) We would like to examine the contention that whether the claim of the Respondents can be rejected merely on the ground of being speculative Investor. In this context we refer to the Judgement of Hon’ble NCLAT in the matter of Everlike Real Estate & Developers Pvt. Ltd. Vs. Mr. Mohit Goyal, CA(RP) and Anr. (2024) ibclaw.in 429 NCLAT, wherein it has been held as under:

“The Hon’ble Supreme Court of India in Pioneer Urban Land (2019) ibclaw.in 13 SC held that the allottee, who has given advance or paid money to the Real Estate Developers is a Financial Creditor. The issue regarding the genuine Homebuyers v/s Speculative Homebuyers is relevant only at the stage for the admission of CIRP under Section 7 of the Code. Thus, it becomes clear that the Hon’ble Supreme Court of India held the position of speculative investors only for seeking unnecessary insolvency of the Corporate Debtor. The Hon’ble Supreme Court held that any allottee who paid for purchasing units will be treated as having effect of commercial borrowing and consequently such unit purchaser will be treated as Financial Creditors. (p49)

Thus, it becomes clear that whether the homebuyer/ allottee is genuine homebuyer or genuine allottee or speculative homebuyers/ allottee but if he has paid the money for acquisition of such properties or given the advance, such allottee/ homebuyer shall be treated as Financial Creditor in terms of Section 5(8)(f) of the Code. Hence, the pleadings of the Respondent No. 2 in this regard that the Appellant is speculative investor will not affect the rights of the Appellant to be treated as the Financial Creditors. (p50).

29) From perusal of the above it is observed that even though the allottee may be falling under the category of speculative investor, it will still be considered as Financial Creditor. In our view the Speculative Investor is barred from initating the CIR Process. However, we don’t find any impediment to treat the Allottees, even if they are speculative investors, from filing their claim and admission of their claim as Financial Creditor in a class. The claim of an allottee cannot be extinguished merely because of being a Speculative Investor. Hence, we reject this contention of the Applicant.

30) Another allegation has been levelled that That Respondent No. 2 and 3 are related parties of CD. Mr. Gurcharan Batra is the erstwhile Director of CD in the year 2014 hence, are related parties. In this regard, it would be apposite to refer to the Reply of Respondent No. 1 as under:

31) That the test of related party has to be seen as on the date of CIRP as held by the Hon’ble Supreme Court in Phoenix ARC Private Limited v Spade Financial Services Limited & Ors (Civil Appeal No. 2842 of 2020 with Civil Appeal No. 3063 of 2020. The relevant excerpts of the Judgement reads as under:-

94. Thus, it has been clarified that the exclusion under the first proviso to Section 21(2) is related not to the debt itself but to the relationship existing between a related party financial creditor and the corporate debtor. As such, the financial creditor who in praesenti is not a related party, would not be debarred from being a member of the CoC. However, in case where the related party financial creditor divests itself of its shareholding or ceases to become a related party in a business capacity with the sole intention of participating the CoC and sabotage the CIRP, by diluting the vote share of other creditors or otherwise, it would be in keeping with the object and purpose of the first proviso to Section 21(2), to consider the former related party creditor, as one debarred under the first proviso.

32) The Applicant has not said anything contrary to the Reply. Further the Reply of the Respondent suggest that they ceased to be the related party in the year 2014 and the CIRP was initiated much after that. Hence we do not find any force in the allegation of the Applicant.

33) The Applicant has further alleged that the claims of Respondent Nos. 2 and 3 are barred by limitation. In this regard, Respondent No. 2 in its Reply has annexed Annexure R-2/1 which is a Reply on behalf of Corporate Debtor in CP(IB) No. 210/Chd/Hry/2020 filed before this Adjudicating Authority in a petition u/s 7 filed by home buyers wherein, both Respondent nos. 2 and 3 are Petitioners. In the said Reply, the CD has taken a categoric stand as under:

“i. On 14.3.2014, in Civil Writ Petition No. 4856 fo 2014 titled as Rupinder Kaur & Ors. Vs. State of Punjab & Ors., Division Bench of Punjab & Haryana High Court was pleased to pass a ‘Status Quo’ order on the project. That the said litigation finally came to end on 16.1.2018. Therefore, in view of the order of injunction/stay granted by Division Bench of Punjab and Haryana High Court, the date of handing over possession of the Project gets automatically extended and there is no cause of action to file the present petition.

ii. New management took over the Project under a ‘Share Purchase Agreement’ and thereafter infused funds/resources in the Project. After the Litigation of the High Court got over in 2018, new promoters under RERA laws submitted the plans and competition date, which is accepted by the authorities that is in June 2022 (subject to COVID related delays. Thus, there is no cause of action to file the present petition.”

34) The allegation regarding the claims being barred by limitation is in the teeth of the above stand of the CD before this Tribunal. Admittedly the date of completion has been extended to 30.6.2022 as per Registration approval dated 17.10.2017 granted by RERA, Punjab (Annexure R-2/11). Hence, there is no merit in the allegation that claims of the Respondent Nos. 2 and 3 are time barred.

35) The Applicant has raised another ground that as per MCA data, Respondent Nos. 2 and 3 have been struck off under Section 248 of the Companies Act, 2013 and hence, their claim cannot be accepted. It is been stated by the Respondents that under Section 250 of the said Act, even if a company is dissolved under Section 248, there is no bar from realizing the amount due to the company and for the payment or discharge of the liabilities or obligations of the company. It has recently been held by the Hon’ble High Court of Delhi in the matter of A.B. Creations and Anr. V. Bhan Textiles Pvt. Ltd., (2024) ibclw.in 1155 HC as under:

“12. What, therefore, follows on a careful reading of the words in Section 250 of the Act by invoking the golden rule of construction that the words in the statute should be interpreted in their ordinary, normal and grammatical meaning, is that even if the name of a company is struck off from the register, it remains operational in so far as it can pursue legal remedies for realisation of the ‘dues’ of the said company against its debtors, which have either crystalised or remain uncrystallised, arising from any liability or obligation of its debtors to the company, but even the creditors can pursue legal remedies against the said company for the payment and discharge of its liabilities or obligations arising from any contract or statutory implications.”

36) In the light of discussion and reasons recorded hereinbefore the application being bereft of merits deserves dismissal. As a result the IA- 2105 of 2023 is accordingly dismissed with no order to costs.

---------------------------------------------------------